“As the 2012 presidential candidates prepare their closing arguments to America’s middle class, they are courting a group that has endured a lost decade for economic well-being. Since 2000, the middle class has shrunk in size, fallen backward in income and wealth, and shed some—but by no means all—of its characteristic faith in the future.”

And here’s the section titled “

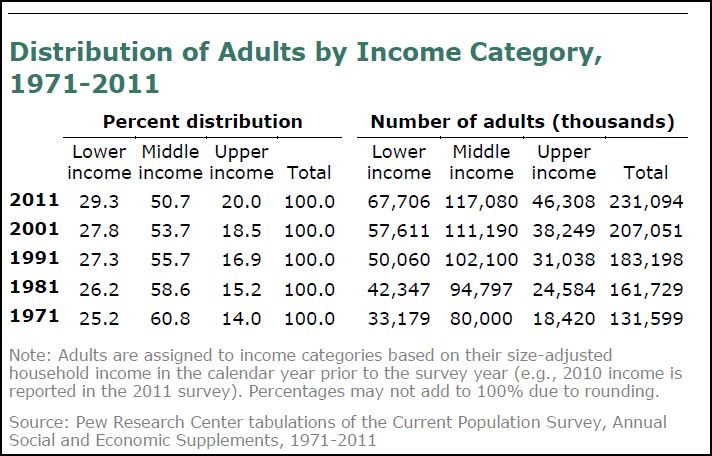

How Many Adults Are Middle Income?” from the

full report (p. 65) which discusses the data in the top chart above:

“The size of the middle-income tier varies over time because the incomes of individual households, in relation to the overall median, vary over time. In 2011, 50.7% of adults (ages 18 and older) lived in middle -income households (see top chart above). In number, that amounted to 117 million adults out of the U.S. household population of 231 million adults. The share of the U.S. adult population that lives in middle-income households has diminished over time. In 1971, 60.8% of adults lived in middle -income households, 10 percentage points more than in 2011 (see top chart).

The shrinking, or hollowing out, of the middle –income tier has been accompanied by an increase in the shares of the adult population at the high and low ends of the

income distribution and roughly equal shares have moved up or down. The

share of the population in the upper-income tier has risen from 14% in 1971 to 20% in 2011. At the same time, the share in the lower-income tier grew from 25% in 1971 to 29% in 2011. Thus, from 1971 to 2011, the U.S. adult population has become more economically polarized with relatively more in the top and the bottom tiers, and fewer in the middle.

The hollowing of the middle -income tier has been a steady and virtually uninterrupted process over the past four decades. Starting from 1970, every decade has ended with a smaller share in the middle -income tier and higher shares in the lower- and upper-income tiers. No single decade stands out as having energized the movement of people out of the middle.”

MP: Here’s a slightly different interpretation of the changing distribution of income in the U.S. between 1971 and 2011:

1. In 1971, 86% of adult Americans were considered either lower-income or middle-income, and by 2011 only 80% of Americans were in those two income categories. At the same time, the percentage of “upper-income Americans” increased from 14% to 20%, reflecting significant upward income mobility during those 40 years as millions of Americans left the middle class for the upper-income group.

2. Between 1971 and 2011, the share of adult Americans in the “middle class” decreased by ten percentage points from 61% to 51%. Of that 10% of American adults who left the middle class, 6% moved up to the “upper-income” category and 4% move down to the “lower-income” category. Alternatively, we could also say that 150 American adults moved up from the middle-class for every 100 adults who moved down from the middle-class between 1971 and 2011. Or we could say that in that 40-year period, it was 50% more likely that an American adult would move up from the middle class to the upper-income group than he or she would move down to the lower-income group.

3. Using the numbers in the bottom chart we could also say that if the 1971 income distribution percentages (25.2%, 60.8% and 14%) hadn’t changed, then in 2011 there would have only been 32.35 million upper-income American adults (14% of 231.1 million) instead of the actual 46.31 million Americans in that category today (20% of 231.1 million). So instead of characterizing the shifting income trend as the “shrinking, or hollowing out, of the middle –income tier,” we could also characterize it as a period of significant upward mobility, during which an additional 14 million Americans moved into the upper-income tier.

Of course, we could also say that if the 25.2% of American adults in the low-income group hadn’t increased to 29.3%, we would have about 9.5 million fewer lower-income American adults today. But like I mention above, about 50% more American adults moved up to the highest group than moved down to the lowest group. In other words, Pew’s statement that “roughly equal shares have moved up or down” isn’t really accurate (6% moving up is not roughly equal to 4% moving down). It would be more accurate to say that it was about 50% more likely that an American adult moved up from the middle class to the upper-income group than moved down from the middle class to the low-income group between 1971 and 2011.

Bottom Line: Far from being gloomy, perhaps there’s a positive story here. A story that over the last forty years there has been significant movement by income category among American adults, as would be expected in a dynamic economy, with movement going in both directions. But on net, the changing income dynamics have been positive overall, with about 150 Americans moving up for every 100 Americans who moved down.