NY Fed Model: No Chance of Double-Dip in 2011

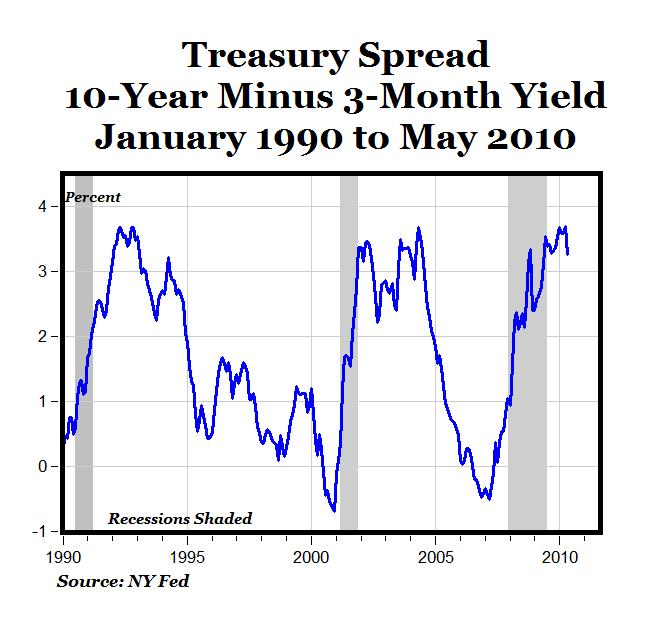

On Monday, the New York Federal Reserve updated its "Probability of U.S. Recession Predicted by Treasury Spread" with treasury yield data through May 2010, and the Fed's recession probability forecast through May 2011 (see top chart above). The NY Fed's model uses the spread between the yields on 10-year Treasury notes (3.42% in May) and 3-month Treasury bills (0.16% in May) to calculate the probability of a U.S. recession up to twelve months ahead (see details here).

The Fed's model (data here) shows that the recession probability peaked during the October 2007 to April 2008 period at around 35-40%, and has been declining since then in almost every month. For May 2010, the recession probability is only 0.17% (about 1/6 of 1%) and by a year from now in May of next year the recession probability is even lower, at only 0.12%.

According to the NY Fed Treasury Spread model, the recession ended sometime in middle of 2009, and the chances of a double-dip recession through May of 2011 are essentially zero.

9 Comments:

This model assumes an efficient market, not one that has been manipulated with enormous purchases of toxic assets by the FED. Specifically, the FED keeps rates at the lower end near zero to artificially push the probability down in a desperate attempt to makes this a self-fullfilling profecy.

I hope that you are correct, Mark. However, your perma-bull perspective on our economy will likely bite you in the butt, since you seem to ignore the fact that we have dozens of radical Marxists throwing monkey wrenches into the works of our system. Chairman Ozero's goal seems to be economic ruin for the US and it's a testament to the robustness of our citizens that he hasn't managed to accomplish his goal. Yet.

look at the spreads.

in 1002 ans 2001, they were showing very low chance of recession until the abruptly spiked right before the recession. the only time that didn't happen was last time.

trying to use this model (even assuming the current inputs are not distorted to the point if uselessness by the feds asset programs) is like trying to use the VIX to predict a stock market collapse. it's a coincident indicator, not one with future predictive value.

nobody in the quant modeling community put's any faith in this model. it showed a <10% chance of recession in 2000. its track record is pretty awful.

that should read 1992.

here's the long term track record:

http://www.newyorkfed.org/research/capital_markets/Prob_Rec.pdf

as can be readily seen, this model was showing recession likelihoods of well under 10% right up to the start of the recessions in 1960, 1974, 1982, and 2001, fully 50% of recessions shown in the record.

82 and 74 took the model almost totally by surprise, both showing liklihoods of under 2% until right when the recession bit.

not terribly confidence inspiring.

The market is so overjoyed at this rosy news it gave back 41 points today.

The TED spread is widening, the VIX is up.

No chance of a double-dip and no chance the Titanic would ever sink. I wish we could chain people's financial and professional futures to their words.

Volatility is much bigger now due to interventionism, expect that ups and downs much closer in time...and probably bigger...

The Fed recession model does not account for the massive Fed purchase of government assets, driving the rates to virtual zero. The model applies to a free market.

The massive tax hikes are a war on business and the economy generally, to say nothing of massive new regulation, and Marxism rhetoric.

If it can get worse, it will. Government intervention ruins everything it touches. There isn't one thing the government has done that has been good for the economy, now or ever. Why don't people understand that the government should not interfere with the brilliance of the private sector to create wealth for everyone?

Post a Comment

<< Home