Due to Popular Demand: Update on the TED Spread

Anonymous: What about the TED spread? It's not looking good lately.

Morganovich: you [sic] will not hear MP discuss the TED spread again as it no longer agrees with his position and i [sic] fear that his use of data is quite selective. but [sic] TED is telling us something (especially with m3 [sic] in deep contraction): welcome to liquidity crunch part 2.

Therefore, by popular demand, the TED Spread is presented in the two charts above. The TED spread is currently at 32.89 basis points as of today, about the same level as the spring of 2007 three years ago, and far, far below the triple-digit levels that prevailed betwen mid-2007 and early 2009. If there's any major credit risk concerns in the U.S. economy, it's sure not showing up yet in the TED spread, which continues to "look pretty good lately."

Morganovich: you [sic] will not hear MP discuss the TED spread again as it no longer agrees with his position and i [sic] fear that his use of data is quite selective. but [sic] TED is telling us something (especially with m3 [sic] in deep contraction): welcome to liquidity crunch part 2.

Therefore, by popular demand, the TED Spread is presented in the two charts above. The TED spread is currently at 32.89 basis points as of today, about the same level as the spring of 2007 three years ago, and far, far below the triple-digit levels that prevailed betwen mid-2007 and early 2009. If there's any major credit risk concerns in the U.S. economy, it's sure not showing up yet in the TED spread, which continues to "look pretty good lately."

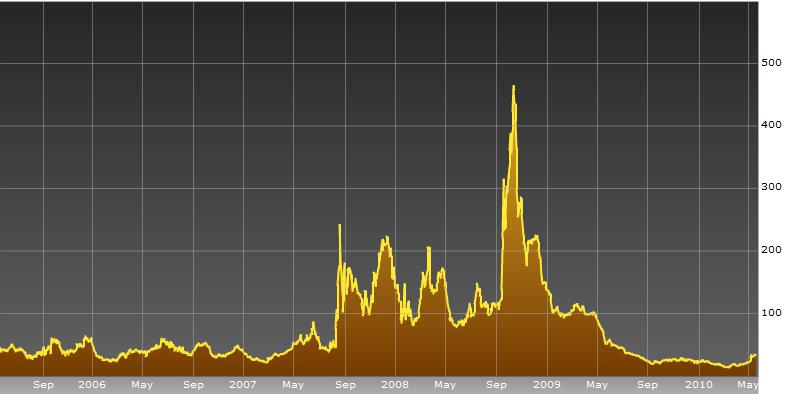

Anonymous: "The market is not worried about the US. It's worried about Europe. Check 1 month LIBOR. It's heading back up past the summer levels last year."

Here's one month LIBOR, it's close to a 20-year low:

13 Comments:

Go to Bloomberg and click on the 5Y button for a better view.

The market is not worried about the US. It's worried about Europe. Check 1 month LIBOR. It's heading back up past the summer levels last year. That's even after that $1 trillion bailout plan was rolled out.

We don't export all that much to Europe, but multinationals have a lot of operations there. Just when revenue was starting to come back, the last thing companies needed was to see revenues and profits from European operations getting knocked down.

We don't export much at all, do we? I agree, the market is not worrying about the U.S.

But, if it's worried about Europe, we should be worried about the U.S. in about ten years' time. We just became the new Europe. The same diseased policies currently crushing Europe will crush the U.S.

The market is not worried about the US. It's worried about Europe.

Well it's a good thing that U.S. financial institutions don't have any exposure to European debt then, or we might be in a little bit of trouble.

LIBOR may be near 20 year lows, but so are many things like automobile sales and housing prices in some states. Yet the change is what we look at for those, to indicate a V recovery.

What does the sharp change in LIBOR mean coming into May? Recovery? Doesn't seem like it. Government bonds are yielding nearly zero and plenty of people are buying those just to get their money back. Some banks are starting to worry that some of their money isn't going to come back.

Try a 1 year view:

http://www.bloomberg.com/apps/cbuilder?ticker1=US0001M%3AIND

Coincidentally, there's an article today about sibor in Singapore popping.

http://www.bloomberg.com/apps/news?pid=newsarchive&sid=aF2mAMPN1i7o

Is it really coincidence that stocks started selling off right as LIBOR shot up? It could be, except the lending environment in Europe was specifically mentioned as a reason investors were worried. There was talk of Lehman 2 out there in Europe, and that flash crash didn't happen in a vacuum.

banks have not been funding themselves in the overnight interbank market since Lehman. TED spread isn't a very useful indicator anymore, notwithstanding the fact that it remains at very low levels by historical standards.

Gherald - that's the six month view! No wonder you lack perspective!

I think this discussion is more eared towards the Libor-ois spread so here I'm linking the chart at bloomberg. I suggest the 1 and 5 year charts but can't seem to link them separately.

http://www.bloomberg.com/apps/cbuilder?ticker1=USSOC%3AIND

i stand corrected, it appears we we will hear about it. thank you doctor perry.

perhaps you'll include the unemployment numbers from yesterday as well? i continue to think you'd do a great deal for the credibility of your analyses if you included the data that disagrees with your V shaped recovery thesis as well.

that said, watch TED (or better, watch LIBOR). it's certainly not at crisis levels yet (30 is about the LT average), but a move from 10 to 30 in 6 weeks with the move from 20-30 coming in just a few days is a bit worrying - fear is creeping back into the interbank system in europe. no one has gone down and the euros are well ahead in terms of at least announcing (if not implementing)a rescue plan, but don't underestimate how different a 30bp spread is now than 2007.

in 2007, US short term treasury yields were around 5%, so a spread of 30bp was about 6% of yield. currently, USTY is more like 14bp. thus, the spread is more than 200% of yield, a less attractive situation for short term borrowing.

another way to look at it is that the cost to borrow interbank is up 50% since march.

ignore that if you like, but seems a warning sign to me, especially with growth slowing and M3 in rapid contraction which is historically a 6 month precursor to economic contraction.

this is all draining the monstrous liquidity that drove the recent bull.

also:

looked at the VIX lately?

16 to 46 in a month is quite a jump. (and back to levels similar to q1 2009)

(though note, vix is a coincident, not a leading indicator)

Are we experiencing a 30 year cycle liquidity crunch? Here is chart comparison between the TED spread and S&P 500 going back over thirty years. The Euro Union needs to inject liquidity to avoid rugged TED mountain range chart!

I hope Professor does not quote me because i'm sure it would make me look "sic".

The market is not worried about the US. It's worried about Europe.

Now why would they be worried about Europe? Hmmm:

Federal Reserve officials took pains this week to dispel any notion that their support of Europe's $1 trillion bailout meant U.S. taxpayer funds would be used to prop up the profligate Greeks. But in explaining the need for it to help ease financial strain, the Fed underscored that big U.S. banks remain vulnerable to Europe's financial contagion.

During a closed-door meeting on Capitol Hill, Fed Chairman Ben Bernanke told lawmakers a European crisis would threaten U.S. banks, Sen. Richard Shelby said after the meeting. In a speech Thursday, Fed Vice Chairman Donald Kohn noted that lending systems "remain somewhat vulnerable."

Euro Pain Could Blow Back on Big U.S. Banks, WSJ

This just in: German parliment approves near trillion dollar rescue plan.

OK, good: there is the liquidity to tame TED spikes. We now need long-term government spending restraits.

Post a Comment

<< Home