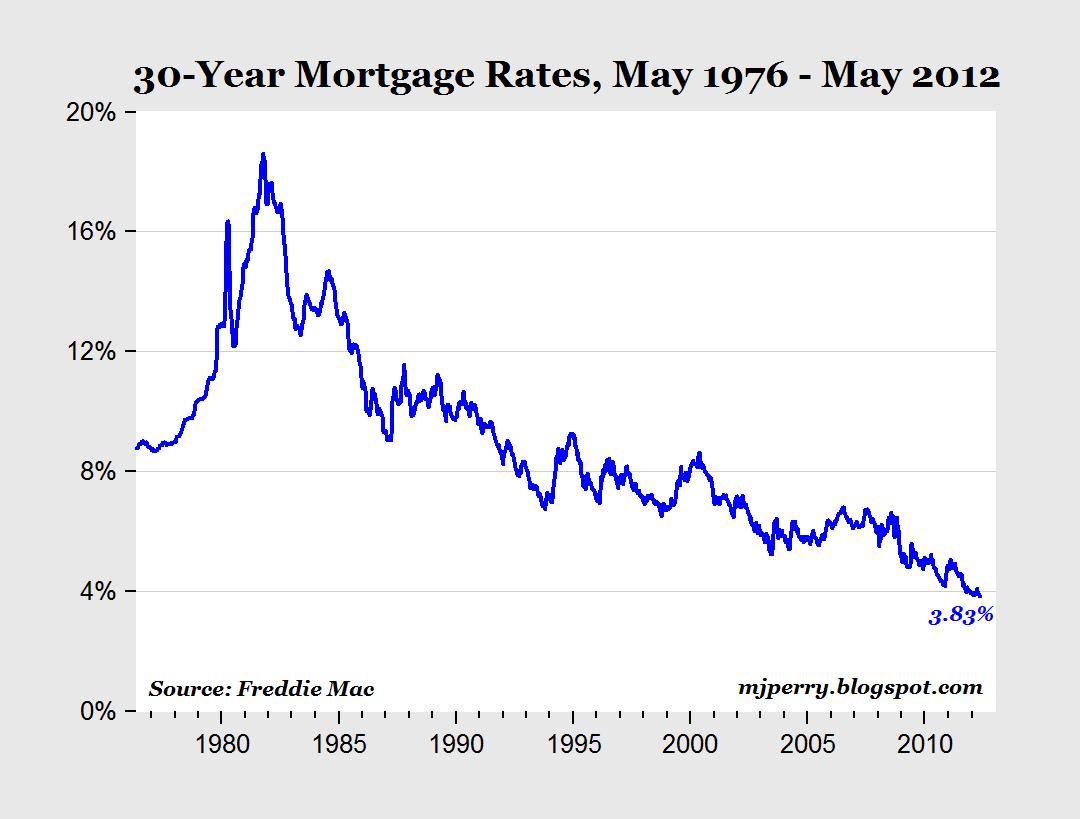

Mortgage Rates Fall to Record Lows This Week

Professor Mark J. Perry's Blog for Economics and Finance

Dr. Mark J. Perry is a professor of economics and finance in the School of Management at the Flint campus of the University of Michigan. Perry holds two graduate degrees in economics (M.A. and Ph.D.) from George Mason University near Washington, D.C. In addition, he holds an MBA degree in finance from the Curtis L. Carlson School of Management at the University of Minnesota. In addition to a faculty appointment at the University of Michigan-Flint, Perry is also a visiting scholar at The American Enterprise Institute in Washington, D.C.

17 Comments:

I guess mortgage lenders are really, really debase.

Can't they see hyperinflation, when it stares them in the face?

Benjamin-

Nice poetry :)

And to think...just yesterday I said "I don't see how mortgage rates can go any lower."

You say that like it's a good thing rather than a sign of central planners doing increasingly desperate things to prop up a sick economy.

Mortgage rates are low, but how many people are able to get a mortgage?

A read in the Freeman a few months ago about how the Fed has both done everything imaginable to drive down the interest rate (mortgages are priced off the 10-year treasury) and imposed stricter lending standards.

The net result is that few people qualify to borrow. Anecdotal evidence suggests the standards for jumbo mortgages and re-refi are crazy.

"I read" Sorry.

benji-

mortage lenders could care less what inflation is.

freddy and fannie are buying up 90% of all origination.

all you have to do as a lender is issue at 4% and sell 2 weeks later to freddy at 3.80% and bingo, instant profit, no risk, take the money and use it to buy levered treasuries.

this has been explained to you time and time again. why do you persist in making the same debunked claims?

this is not a sign of inflation expectation, just like the bond market, it's a sign that there is a massive greater fool deliberately distorting prices.

(note that the fool in both cases is a federal agency)

Lots of people desire mortgages, but do not qualify -- the low interest rates are not about attracting people in need of mortgages -- the low interest rates are a side effect of some much worse happening in the economy...

also realize-

the bond market price manipulation feeds into the treasury's ability to fund such cheap loans at F+F.

consider:

if the fed and increased leverage keeps bond yields at 3%, then the treasury can lend profitably at 3.8% through the now nationalized GSE's. sure the fed is left holding the bag and the banks with far more leverage, but hey, they got free money at zero risk for acting as originators and likely get paid to be the servicer as well.

sure, it just perpetuates the govvies debt bubble and just makes the impending bursting of it more painful when it comes, but what has this fed done in the last 20 years that would lead anyone to be surprised by their pursuing a strategy of kick the can down the road?

these are not price signals given off by a free market, they are prices set by federal agencies in a deliberate attempt to prop up a market.

W.C. Varones: I'm just reporting this because it's a new all-time historical record-low for both 30-year and 15-year mortgage rates. It's more for historical significance than any editorial viewpoint.

mortgage rates might be low but commercial loans of any size are still not particularly easy to get right now.

Spec commercial south of the DC area still has a lot of vacancies.

but something must be happening:

Fannie Mae posts biggest profit since 2007

I know... just teasing :)

http://www.steelheadcapital.com/rates.asp

Morgan--

You make a good point---but even commercial mortgage are way down, with no government resale market.

7 year commercial mortgage money for 4 to 5.8 percent.

So, commercial mortgage lenders obviously do not anticipate hyperinflation.

They may be wrong---I am only saying that institutional players do not anticipate hyperinflation.

benji-

we've been through this as well. the commercial loans are driven down by the same factors as the bond market.

if the cost of capital is low (as it is in every prime bond market due to qe, twist and zirp) then the banks are just playing the spread.

borrow at 2.5% for 10 years and give out commercial loans at 5% with matching duration.

this offset makes them inflation neutral. works the same with inflation at 3% or 30%. they are just taking the spread.

it's not that different with deposits either.

they are not lending their own money. it's your money. if you come back in 10 years and your dollar now only has 50c or buying power, well, that's your hit, not theirs. they have just been taking a % gain while your asset depreciates.

i do not think these rates provide the signal you are thinking they do.

just like a bank can keep getting interest and making money from your mortgage while you lose on the value of your house drops, then can do the same renting out your money while you take the hit due to inflation.

Morgan-

Look ultimately, if institutional lenders believe a hyper-inflation is coming, you will not be able to borrow for low, single-digit rates.

Banks cannot get enough capital from merely retail accounts. And anyway, even retail depositors would not leave their money in a bank at 1 percent interest if they thought hyper-inflation was present or coming.

I just don't see how interest rates stay low into the teeth of hyper-inflation.

Look, the capital markets could be wrong. We may have hyperinflation next year. I am saying both retail and institutional lenders are not acting as if they anticipate that. They lend as if they anticipate low inflation.

I see a more Japanitis situation, and perhaps fitful deflation, or very low inflation.

We have a difference of opinion, but I enjoy reading your comments.

benji-

"Look ultimately, if institutional lenders believe a hyper-inflation is coming, you will not be able to borrow for low, single-digit rates."

that is simply untrue.

if i can borrow for 10 years at 2.5% and lend to you at 5%, why would i care what inflation is? every bit of value i lose on your less valuable dollars in 10 years, i recoup by paying back less valuable dollars to the guy i borrowed from.

it's just a rate spread. inflation at 1% or 100% makes no difference to the profitability.

banks have tons of capital from retail accounts and they are getting most of it bank from freddy and fannoe right after they lend it. banks are SWIMMING in capital right now. that's the other reason rates are low.

the bank lends to you, the loan gets solf to F+F, then they have to put the money to work again. the amount of money competing for a few commercial loans is massive.

again, the rates you are trying to use as a signal of inflation expectation are nothing of the sort. they do not have anything to do with inflation and cannot be used as market signals in the manner you are attempting to.

it's like trying to use your oil temperature gauge to determine how fast you are going. it just does not work.

This is a great example of how weak the economy is. Does anyone believe that the Fed would be keeping rates low if there were any hope of a recovery in the near term?

I cannot believe that 30 year home mortgages are at 3.69%. Could you please repeat that. Now if 30 year mortgages at 3.69% cannot get the housing market going. I don't think anything can.

Post a Comment

<< Home